Issue 1A revenue helped push Arapahoe County fund balance to $151.4 million

Arapahoe County’s unassigned general-fund balance rose $88.9 million from 2023 to 2025, as Issue 1A-related revenue and restrained spending increased reserves. Officials say the jump is not recurring operating revenue and will be phased into capital projects.

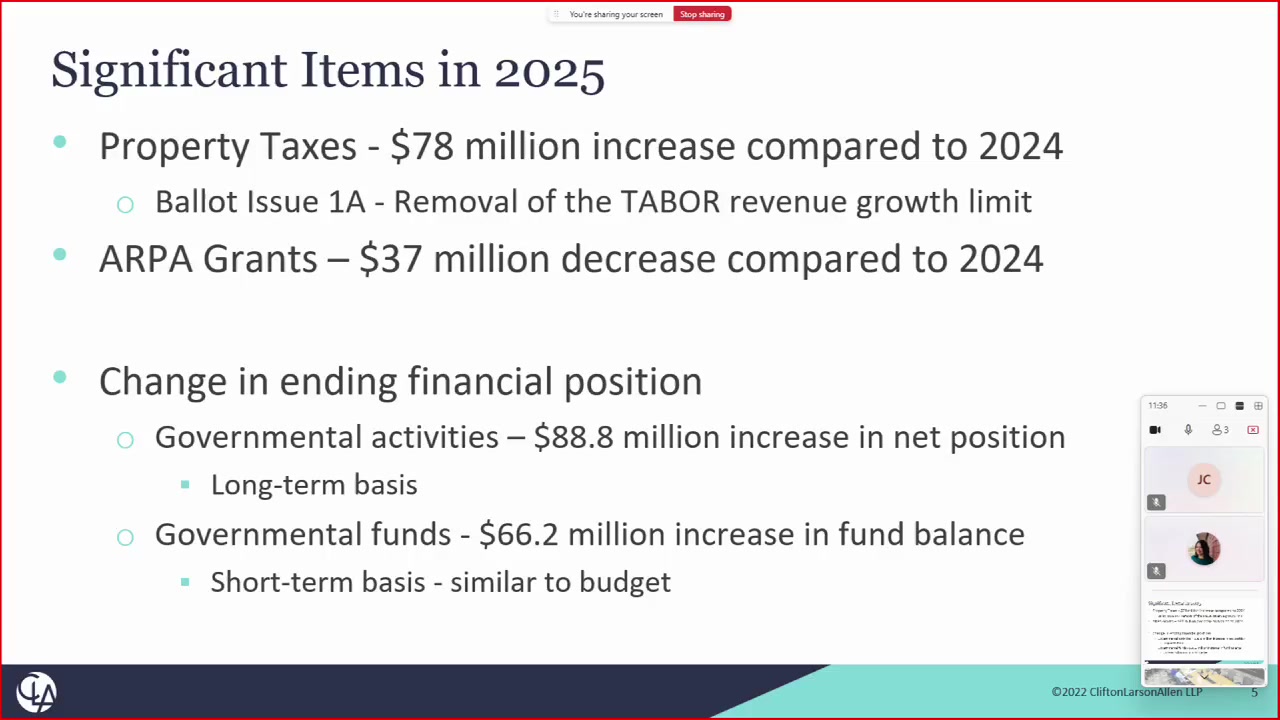

Arapahoe County’s unassigned general-fund balance rose from $62.5 million in 2023 to $151.4 million in 2025, an $88.9 million increase disclosed when commissioners received the county’s fiscal 2025 financial report and audit results July 14. Roughly $78 million in additional property-tax-related revenue, tied largely to voter-approved Issue 1A, drove much of the increase.

CliftonLarsonAllen issued an unmodified, or clean, opinion, with no financial-audit findings or recommendations. The county also reported no findings in its federal single audit, which was required because the county received more than $100 million in federal awards, the board’s study-session record shows.

The balance increase does not represent $88.9 million in recurring operating revenue. County officials said the 2025 jump came largely from the first-year effect of Issue 1A and restrained spending. The measure released the county from TABOR revenue and spending limits, creating continuing authority to retain and spend additional revenue, the county’s explanation says.

Officials said only a small portion of the increase was spent in 2025 as the county prepared its 2026 budget, and that the money would be used over several years. The board has committed to $25 million annually for capital projects, but the July 14 presentation did not provide a project-by-project allocation or show how much of the balance has been earmarked through future budget decisions.

Residents can track the practical effect through the county’s budget and capital-appropriation process. The July 14 presentation was not a final 2027 budget or comprehensive capital-plan vote; upcoming actions will show which projects receive the annual commitment and whether recurring operating costs are supported by recurring revenue rather than the one-time reserve increase.